All categories

Featured selections

Trade Assurance

Buyer Central

Help Center

Get the app

Become a supplier

(1737 products available)

Ready to Ship

Ready to Ship

Ready to Ship

Ready to ShipThere are three main types of bank queue systems that are used by various financial institutions to optimise service delivery to clients. They are as discussed below.

This is a manual ticketing system where clients pick numbered tickets from a machine or take one from a counter. The number is then called either by an employee directly addressing the client or by a screen placed strategically in the bank. The further this system progresses, the more inefficiencies and the need for immediate solutions arise with increasing client volumes, service complexities, and the increasing need for more modern technological interfaces.

With this system, clients can reserve their place in the queue using their mobile devices or computers instead of physically waiting in line. They are able to check the status of the queue, their estimated wait time, or even a real-time update. This system is still relevant because financial institutions have to offer all of their financial customers online services. In the 21st century, when everything looked like it was going to be done on the internet, no one wanted to waste time standing in physical queues, and it was enough to be informed about the virtual one.

This system includes sophisticated hardware, such as sensors and screens, and software applications that automatically assign service numbers to clients, track their status, and analyse data related to queue metrics. The development and installation of these systems entail considerable time and financial costs, although the advantages they provide in terms of increasing clients' satisfaction and financial institutions' effectiveness can offset these costs in the long run.

A queue management system identifies and registers important operational functions. They include the following.

Customer Service Optimization

The core function of a bank queue management system is to improve the flow of clients visiting the bank to receive services. This is being done by eliminating the long and undesirable lines that make the waiting periods seem interminable. The system permits customers to join virtual queues, which release the demand for in-person queuing. It provides a better satisfaction rate among all customers.

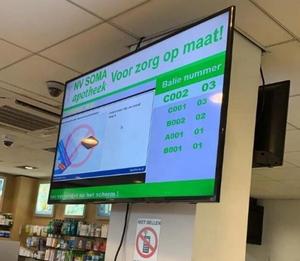

Real-Time Queue Monitoring

Most modern bank queue systems come equipped with features that facilitate real-time observation of the queue. Bank managers can, for example, observe the number of clients in a line, the amount of time each client has been in line, and the situation of the teller for efficient deployment. This awareness allows management to evaluate operational effectiveness and make timely decisions regarding resource allocation.

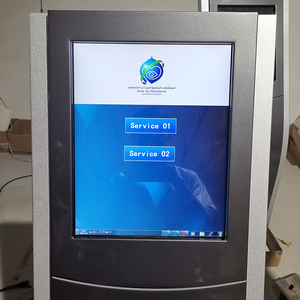

Ticket Issuing and Calling

In traditional queuing systems, customers are usually given tickets that bear numbers, which are their order in the queue, and availability on the system when it is time to serve them. This function is very important since it brings order to the queuing and allows the customers to carry on with their daily business without necessarily being tied to the actual queue. In addition, their screen notifies them when it is their turn to be served.

Data Collection and Analysis

Bank queue systems are closely related to a number of performance metrics that are useful in evaluating banking services. These parameters may be average waiting time, customer traffic at certain times of the day, and the efficiency rate of the teller. This data can be very useful for financial implementations for future planning, identifying areas that require improvement, and enhancing the customer experience.

Bank queue systems have some key features. They include.

Real-time Queue Tracking

Bank employees and management can watch the line as it develops in real time through the provision of this functionality. They can thus see the number of clients waiting, the time taken by clients to wait, and the status of the employees serving those clients. Such visibility can enable better management of resources with the aim of reducing customers' queues and the time they take to receive services.

Customer Notifications

This limits how long customers can wait by enabling systems to inform them of their turn when their number is called via text message or email. Banks can, for instance, notify customers through their mobile application or SMS that their turn is up and that they should report to the nearest banking hall. Customers will no longer wait in vain and can plan their time well while providing a much better customer experience.

Mobile Queue Management

In this feature, customers can join a virtual queue through the bank's mobile application or web portal. This is of great importance to customers since it gives them the ability to hold their place in the queue from anywhere, be it from home, a nearby restaurant, or even while using their business online. This feature introduces convenience and improves customer experience, especially during peak hours when their lines are the longest.

Employee Dashboard

This is an integral component of the system that allows bank employees to check the queues and serve the customers. It presents employees with all the data needed for managing the queue by providing the current state, any active requests, and the service needs of each customer. It is also possible for employees to use the dashboard to measure several parameters so that they can make informed choices regarding staffing and service enhancement.

Coming up with a system that maintains a Bank Queue involves using some specific design aspects. They include.

User Interface and Experience Design

This should be done with a lot of emphasis placed on the user interface, especially those systems that have online queuing components. Customers should be able to easily use the queue management system because they should be able accessing it via a straightforward, quick, and friendly mobile application or web portal. Financial institutions need to put in place good designs because the overall customer experience will depend upon how easy and satisfying it is for the end user to interact with the queuing system.

Integration with Existing Systems

The design of a bank queue system should ensure that the system works with other systems used at the bank, including customer relationship management (CRM) systems) and core banking systems. This can help the bank deliver better services by ensuring that clients' data and other service requests are smoothly transferred from one system to another. Integration means that the queue management system can be easily plugged into the existing technology infrastructure.

Scalability and Flexibility

The bank queue design should be scalable to accommodate future growth in customer base and demand for banking services. This would mean introducing more sophisticated queuing models or functions to correspond with the unique service type. The more flexible the design, the more likely it will respond to changes in the business environment and that it will accommodate new features as they come about.

Data Security and Privacy

Any design in the bank queue system should pay much attention to the issues of data security and confidentiality. Because customers will be using their mobile apps to interact with the queue system, banks have to ensure that sensitive customers' information is well protected. Banks have to comply with the set standards, such as the General Data Protection Regulation (GDPR) and other relevant measures, to gain and keep customers' trust and confidence.

There are several operational scenarios where customer queue management systems can improve bank performance. They include.

For example, a bank may have set hours of the week when its customers are at the bank in large numbers to conduct business. Such days are usually when there are check deposits, payments, or major financial transactions. Without a queue system, the customers would ether experience long lines with no movement at all or, worse still, an overworked staff who is shut up in a small room trying to service clients as she services more clients. However, if the virtual queue system had been in place, customers would have the option of joining a queue through their mobile phones that day, primarily to alleviate the congestion that may have been experienced.

Suppose a certain bank is opening a new branch in a specific location. It has probably gauged the demand for easily available banking services in a given area, and it is consequently providing this branch for any of its clients who so wish to access it. Banks can implement an automated queue management system right from their operation's start to ensure that the inflow of customers is controlled and that the services offered are of quality. This system would allow the bank to gather real-time data about the customers and provide reports that would be helpful in the future.

In this situation, banks offer clients the option of making appointments through their mobile app for personal banking services with a financial adviser or investment specialist, for example. This holds several advantages to the bank since the clients would be attending an appointment rather than queuing up in the banking hall. A virtual queuing system would allow the clients to book the time slots through which they would be able to see the bank advisers. This is also beneficial because it helps cut on the time taken in case the clients are seeking a specific service and also helps improve the service delivery.

If a certain financial institution has a branch in an area where there is a high volume of business activity, it is understandable that there will be times when there are long lines as there is high traffic. Under such circumstances, the combination of conventional queuing systems and high-tide banking activities can lead to disorganization and considerable time wastage. Fortunately, there are virtual and automated queue management systems that can ease congestion by enabling real-time observation of the flow of customers.

Selecting the correct supplier for the bank queue system is essential to implement a successful management system. Here are some factors that financial institutions should consider when selecting a supplier.

Industry Experience and Expertise

Suppliers with industry experience in the banking and financial services sector will well understand the unique challenges and needs of these institutions. They have likely worked on different projects and even come up with solutions that work for other banks, making it possible for them to draw experience from such.Custom Queue Management Systems are designed for you if the Service Provider has numerous years of experience working with high-stakes clients.

System Customisation

Every bank has its own distinct way of operating, and a good bank queue system should address its specific needs. Check how flexible and customizable their queuing system is - can it be personalized to reflect the uniqueness of your brand, for instance, in the online queuing system, customer categorization, and reporting dashboards? This will guarantee high quality in functionality and a high rate of customer satisfaction based on how well the system fits in with the bank's operations.

Technical Support and Maintenance

Technical Support and MaintenanceThis work will ensure that the queuing system will always function as it should. It should be possible for the supplier to deliver on-site support, remote support, telephone support, and well-structured guarantees so that any operational breakdown will be handled with as little time loss and inoperability as possible. Furthermore, the speeds of interventions and accessibility of spare parts must be checked, as unavailability of these might lead to massive inconveniences in the banking operations.

Cost and ROI

Although it is important to consider the cost of purchasing and installing the queuing system, it should not be the only one. Instead of just going on the cost that has to be incurred on the system, consider the investment returns: what reduction will be in the customer's queuing time? What will be the increase in the efficiency of the employees? The value the system adds to the bank will, in the long run, outweigh the costs in the long run.

Technology and Innovation

The queuing systems have changed quite a lot due to the introduction of new technologies, mainly due to the introduction of mobile queuing and analytic-based systems. When picking a vendor, ask whether they developed any broad-based technology, particularly for banks. They should offer additional features, automated queue management based on artificial intelligence, and consistent system integration to improve service delivery.

A1: A bank queue system is important due to several reasons. First, it improves customer experience by reducing their time of wait. Second, it increases the efficiency of the bank operations by ensuring that the available resources are optimally utilised. The system also improves the processing capability during peak times and provides data that can be used to enhance future planning and management.

A2: The elements of a virtual bank queue system include customer registration through an application or web portal, real-time status updates, and customer notification by mobile phone or email when it is their turn to be served. With these features in place, banks will be able to provide their clientele with even more convenience, thereby improving customers' already satisfactory experiences.

A3: In the automated queue system, customers are identified and served using modern technological hardware and software with minimal human interaction. Automated systems have high accuracy and efficiency and require little to no physical interaction with customers, further enhancing the customer experience.

A4: Yes, most bank queue systems can integrate with existing banking technologies. Such systems are designed to work with core banking, customer relationship management, or other software that has been previously implemented. This leads to operational efficiency, whereby data is exchanged across the systems and the services enhanced further.

A5: Several factors must be considered for the effective selection of a bank queue system supplier. These include the suppliers' experience in the banking sector, the level of customisation available, the support provided, the quality of the service and the cost as well as the potential return on investment.